You just had a big RSU grant vest. Congratulations — and now the awkward part: a six-figure pile of your own company's stock, a vague sense you should "do something," and no one actually telling you what. An advisor, a spreadsheet, and a piece of software each handle this moment differently. Here's what a modern money tool surfaces in a moment like this — using Ed as a worked example — so you can decide what kind of help actually fits.

Key takeaways

- A money tool's first job isn't to categorize your spending — it's to tell you whether your money could survive a bad month.

- RSUs vest as ordinary income, but employers usually withhold a flat 22% — often below a high earner's real bracket. The shortfall quietly becomes a bill in April.

- After a few years of vesting, a large share of your net worth can end up in one stock. Seeing that number is the point; trimming is your call.

- The honest analogy: a financial advisor's first conversation — without the asset minimum.

- Takes a few minutes. Run a free check-up →

Step 1 — You link your accounts, read-only

You connect your brokerage and bank through read-only aggregation, so the tool can read balances but can't move a dollar. Ed's framing is simple: precise about your money, blind to your identity.

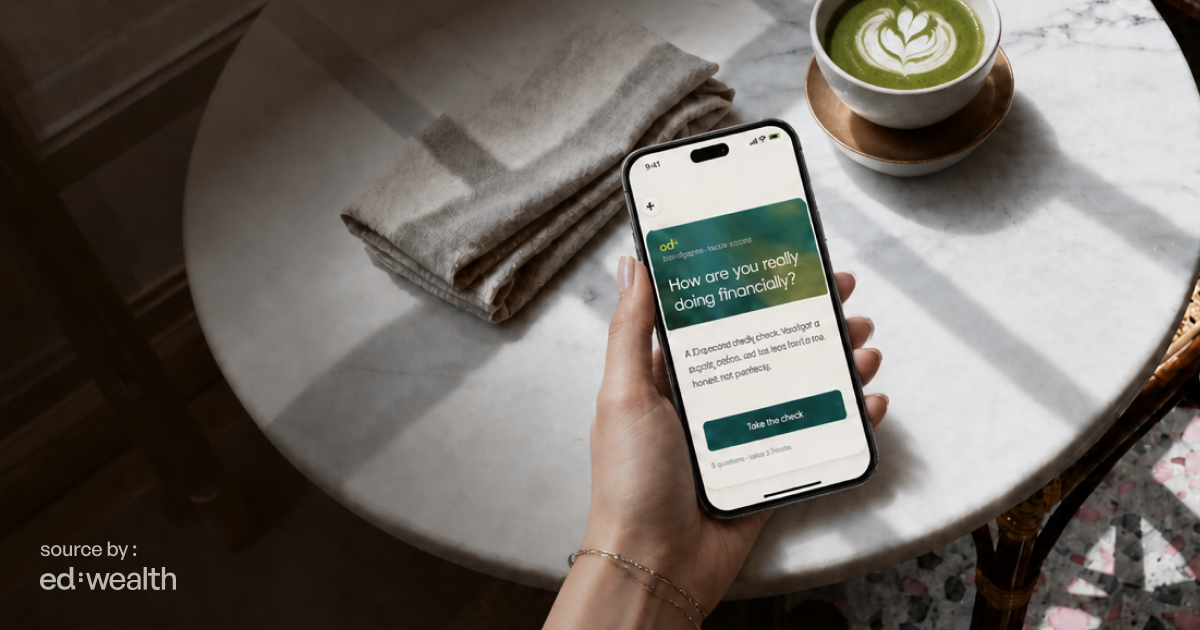

Step 2 — The first screen isn't a spending pie chart

Instead of sorting your lattes into categories, Ed opens on a single Financial Reality Check — a read on whether your money could survive a bad month. For a lot of high earners, that one number lands harder than any budget, because it answers a question the other apps never ask. (If the Reality Check is the numbers side, your money type is the behavior behind them — the two together are the full starting point.)

Step 3 — It surfaces the tax gap most people miss

RSUs vest as ordinary income, taxed like salary in the year they vest (IRS). But the standard federal withholding on a vest is a flat 22% — rising to 37% only above $1 million in a year (IRS Publication 15). If your real marginal rate is 32% or 35%, that 22% isn't "taxes paid" — it's a down payment, and the difference waits quietly until April.

| At vest |

Standard withholding |

A high earner's real bracket |

The gap that waits for April |

| Taxed as ordinary income |

22% flat |

up to 35–37% |

10–15 points under-withheld |

Ed's Tax Check-up surfaces that gap between the 22% standard and your actual bracket; your CPA fills in the exact number. (And if you also exercise ISOs, the alternative minimum tax is a known risk worth raising with that CPA — not something to guess at.)

Step 4 — It makes your concentration concrete

After a few years of vesting, it's common to wake up with a huge share of your net worth in one stock — the same company that already pays your salary. Ed shows your concentration percentage — the share sitting in a single position — and surfaces the question of a cap. When, or whether, to trim is entirely your call; the value is seeing the risk clearly instead of discovering it by accident.

Step 5 — It puts resilience before returns

Rather than jumping to "what should I buy," Ed surfaces a runway shortfall first — the months of expenses that keep a layoff from becoming a crisis — before any investing question comes up. Floor before upside, in that order.

Here's the real differentiator: before you connect anything, you can watch Ed's own live account — unpaid, in public. Most fintech apps hide their numbers; Ed shows his. For a decision this size, "watch mine before you trust yours" is a very different starting point than a marketing page.

What it's good at — and what it's not

The strength is the whole picture: cash, equity, tax exposure, and concentration on one screen, plus a tool honest enough to name what it can't do instead of faking certainty.

What it's not: it isn't a robo-advisor that allocates for you, it isn't a budgeting app, and it doesn't replace your CPA on the exact numbers — it surfaces the questions and hands the precise math to a professional.

Who it's for: high earners with equity and scattered accounts who want to see the whole thing in one place. Who should skip it: if you just want spending categories, or a hands-off robo that allocates and never explains itself, this isn't that.

How it compares

Versus a budgeting app, the difference is direction: those look backward at what you spent; this looks forward at what to weigh next. Versus a robo-advisor, a robo just allocates a portfolio, while Ed reasons across cash, tax, and concentration together. The closest honest analogy is a financial advisor's first conversation — without the asset minimum.

The bottom line

For an RSU windfall, the value isn't a magic answer — it's seeing the whole board before you move. Run a free check-up, see your Financial Reality Check, and watch Ed's live book first.

See where you actually stand → · Ed is available on the App Store.

Partner content, produced in partnership with Ed: Wealth. Educational only — not financial, investment, or tax advice; for your exact numbers, see a CPA. Ed: Wealth is a research and self-reflection tool, not a registered investment advisor. Tax rates and withholding are illustrative.

Sources

- IRS, Publication 525, Taxable and Nontaxable Income (RSUs taxed as ordinary income) — https://www.irs.gov/forms-pubs/about-publication-525

- IRS, Publication 15 (Circular E), Employer's Tax Guide — supplemental wage withholding 22% / 37% — https://www.irs.gov/publications/p15

- IRS, Topic No. 427, Stock Options & Alternative Minimum Tax (ISOs) — https://www.irs.gov/taxtopics/tc427